From Hormuz to household finance: How global oil shocks can filter into Indian homes

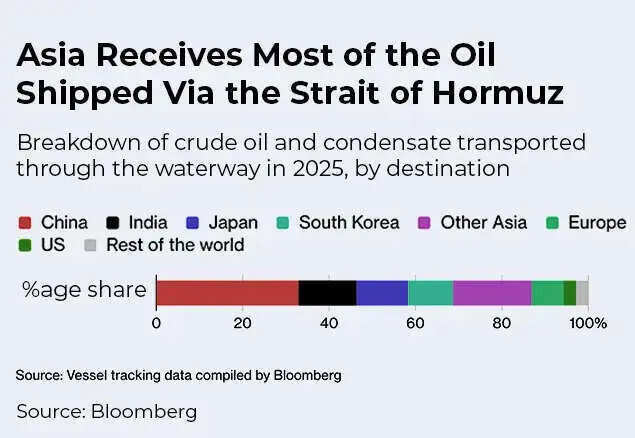

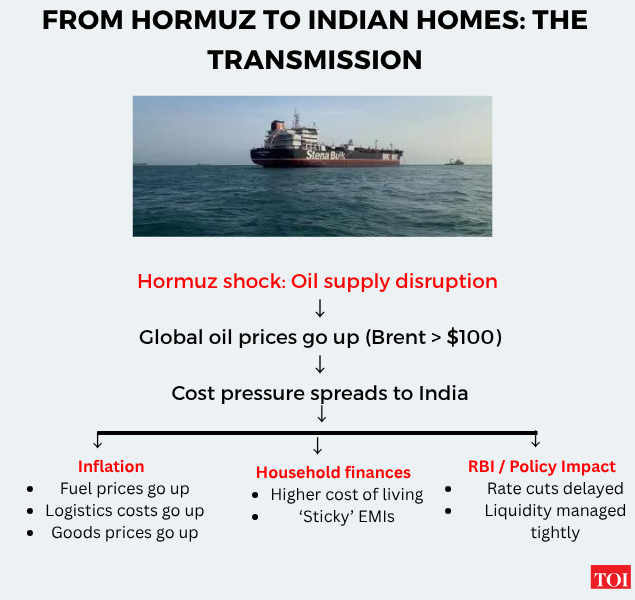

The Iran–US conflict has pushed global oil markets into turmoil, with tensions still simmering despite a two-week ceasefire window, since April 8, intended to enable negotiations. The peace talks amid the fragile truce have so far failed to yield any breakthrough, though diplomatic sources indicate preparations for a second round of talks are already under way. The standoff nevertheless has spilled into one of the world’s most critical energy chokepoints. The US began enforcing a naval blockade around the Strait of Hormuz, targeting vessels linked to Iranian oil exports and disrupting traffic through a narrow corridor that carries nearly 20 per cent of global crude supply.The US naval blockade, imposed this week after failed peace talks, has compounded earlier disruptions by directly targeting Iranian exports and turning back vessels moving through the Strait of Hormuz.However, in the most recent development on Friday, Iran declared the Strait of Hormuz “completely open” to commercial vessels for the duration of the Lebanon ceasefire, marking a temporary easing of tensions in the key global energy chokepoint. However, the relief from the reopening will take time to filter through global markets as freight flows, pricing, and risk premiums adjust gradually, while the effects of the earlier disruption continue to work through the system. The durability and effectiveness of the truce will ultimately depend on how sustainably current arrangements hold, shaping the overall impact of this move.

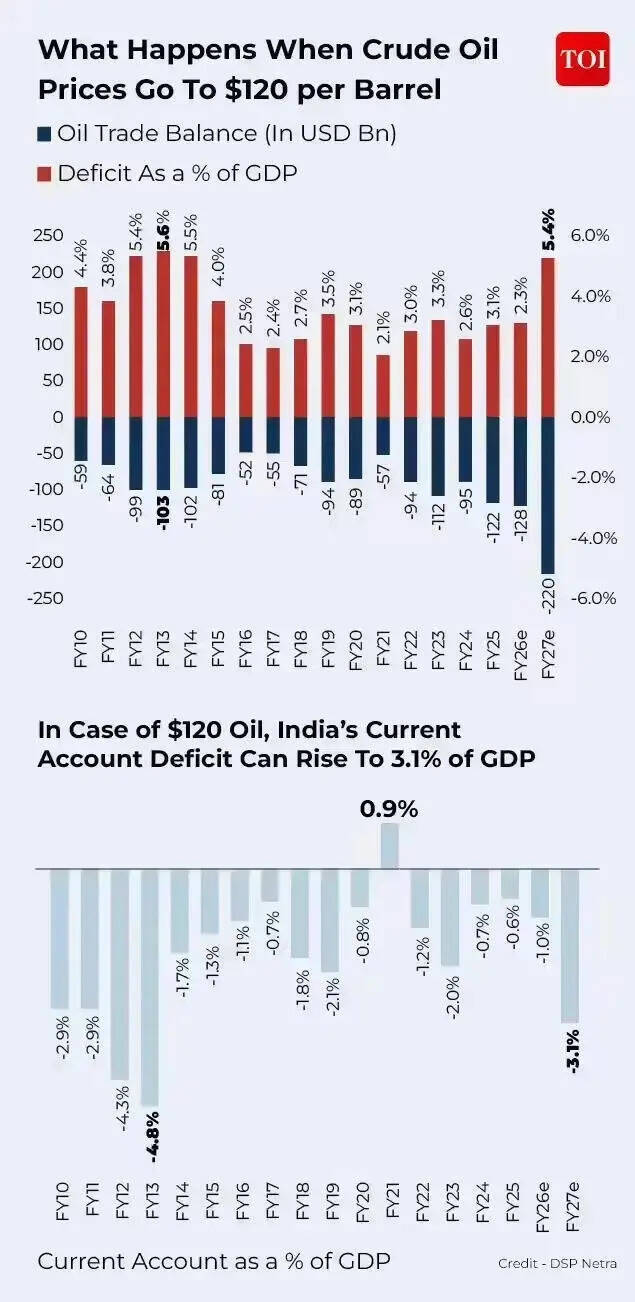

The result is a layered supply shock. Brent crude has swung past the $100 per barrel mark at multiple points during the crisis, reflecting not just immediate supply constraints but a sustained risk premium tied to prolonged instability in one of the world’s most critical oil corridors.For India, the developments are more than a distant geopolitical flashpoint. The country imports over 80 per cent of its crude oil requirement, with a significant share routed through the Gulf. Any disruption,whether a full blockade or even tighter enforcement,feeds directly into domestic costs.What begins as a military and strategic confrontation at sea quickly sets off an economic chain reaction: from crude oil to fuel prices, from fuel to inflation, from inflation to interest rates, and ultimately into household finances.

Oil shock to inflation: The first link

India’s heavy reliance on imported oil makes it sensitive to global price swings. It’s like a 2025 Reserve Bank of India study estimated, that a 10 per cent increase in global crude oil prices could raise headline inflation by around 20 basis points, although the actual impact depends on fuel taxes and pricing decisions.

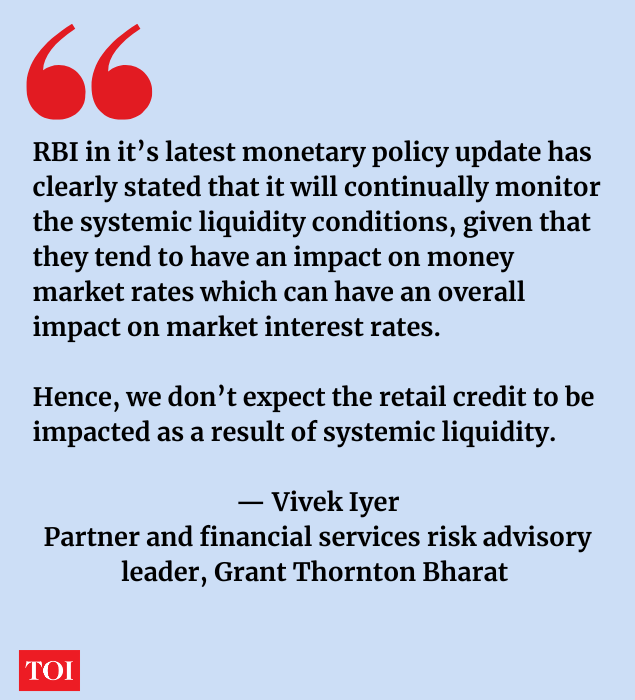

Petrol, diesel, and LPG prices respond first. But the broader impact is felt through logistics. Higher diesel costs raise freight rates, which in turn increase the price of everything from vegetables to consumer goods.Within weeks of sustained price increases, these pressures begin to show up in headline inflation.However, the transmission into core inflation, excluding food and fuel, is less immediate and depends on how deeply cost pressures spread across sectors.This was explained by Vivek Iyer, Partner and Financial Services Risk Advisory Leader at Grant Thornton Bharat, talking to TOI, “Core inflation is a function of demand side shocks or supply side shocks. The RBI monetary policy is usually used to address the demand side shocks and the fiscal policy to address the supply side shocks. The geopolitical tensions will have an impact on headline inflation but don’t see an impact on core inflation as the domestic growth story for India continues to be strong.”

The RBI’s response: Watching, not reacting

Since tensions around the Strait of Hormuz began escalating in late February, the Reserve Bank of India has not taken any oil-specific action but it has adjusted its stance to manage the resulting financial volatility.The central bank has maintained its policy rate unchanged through this period, even as global crude prices turned volatile, signalling a preference for stability over reactive tightening. At the same time, it has stepped up liquidity monitoring, with periodic interventions in money markets to keep short-term rates aligned with its policy corridor.In its latest policy communication, the RBI flagged global commodity prices and geopolitical risks as key uncertainties for the inflation outlook, indicating that external shocks, rather than domestic demand, are driving current price risks.

That distinction matters. When inflation is imported through oil rather than generated by overheating demand, central banks tend to avoid aggressive rate hikes that could unnecessarily slow growth.As Vivek Iyer of Grant Thornton Bharat said, “We don’t expect the interest rate to be on a higher side, as in a globally slow economy and with growth for India being domestically driven, RBI will take a measured approach while keeping a close watch on how inflation expectations evolve.”Thus, the implication is clear: while rate cuts may be delayed, a sharp tightening cycle remains unlikely unless oil shocks begin to feed more persistently into core inflation.

The three levers: How central banks respond

So far, the Reserve Bank of India has held policy rates steady and focused on managing liquidity, even as crude prices turned volatile amid disruptions around the Strait of Hormuz.But if oil prices remain elevated—or spike further—policy choices could begin to shift. Central banks typically respond through three channels, and early signs of some of these are already visible.1. Delayed rate cutsMarkets had begun pricing in a gradual rate-cut cycle earlier this year, particularly after the Reserve Bank of India held rates steady in its February 2026 policy review while signalling comfort with the disinflation trajectory.However, that outlook has become less certain since late February, as tensions around the Strait of Hormuz began disrupting oil flows and pushing crude prices higher. In its April 2026 policy communication, the RBI flagged global commodity volatility and geopolitical risks as key uncertainties, effectively tempering expectations of near-term easing.If crude prices remain elevated:

- Expected relief on EMIs will be delayed: Rate cuts that were earlier anticipated in the first half of the financial year could be pushed further out.

- Borrowing costs not come down for longer: Even without fresh hikes, banks are likely to keep lending rates elevated in line with the RBI’s cautious stance.

- The easing cycle could shift further into the year: Policy may prioritise inflation stability over growth support until oil-driven pressures show signs of easing.

2. Higher-for-longer interest ratesEven without fresh rate hikes, central banks can signal caution—and that shift is often enough to keep financial conditions tight. This dynamic is already visible in market expectations as crude volatility complicates the inflation outlook.A recent example comes from the US Federal Reserve, which through 2024 repeatedly pushed back expectations of rate cuts despite easing inflation. The result was a sustained period of elevated global borrowing costs, as markets adjusted to the idea that rates would stay higher for longer than initially anticipated.A similar pattern could play out in India.If inflation risks linked to oil persist:

- Lending rates are likely to stay higher: Banks tend to price loans off policy expectations, not just current rates.

- Borrowing costs will not come down: From home loans to personal credit, interest costs may not ease quickly.

- Discretionary consumption could soften gradually: With EMIs and credit costs not coming down spending on non-essential goods may not go up and may even see softening if prices go up

This “higher-for-longer” environment does not require active tightening. It works through signalling, where central banks hold rates steady but communicate enough uncertainty to prevent markets from pricing in early easing. What is important to note is that RBI has already cut repo rate by 1.25% in this easing cycle, but the ongoing conflict will delay further rate cuts, in effect dampening hopes of lower EMIs and borrowing costs.3. Tighter liquidity conditionsCentral banks can also respond to persistent inflation by reducing the amount of money circulating in the financial system.In India, the Reserve Bank of India has used this approach in past tightening phases. During the inflation surge in 2022 and 2023, the RBI began withdrawing the excess cash that had been pumped into the system during the pandemic.It did this by encouraging banks to park more money with the central bank through instruments such as variable rate reverse repo (VRRR) auctions. In simple terms, banks had less easy cash to lend, and the cost of borrowing in short-term markets began to rise.This meant that even before the full effect of interest rate hikes was felt across the economy, borrowing was already becoming more expensive at the margins.A similar approach could come into play again if oil-driven inflation persists.This can happen through measures such as:

- Selling bonds to absorb excess liquidity

- Increasing reserve requirements for banks

- Actively managing surplus funds in the banking system

Unlike interest rate changes, liquidity tightening works in the background. But as seen in earlier cycles, it can still push up borrowing costs and slow credit growth across the economy.

That said, the Grant Thornton partner noted that while the RBI continues to monitor systemic liquidity given its influence on money market rates, this may not directly translate into tighter retail credit conditions.

The key shift: Subtle tightening without rate hikes

The current phase is not one of aggressive policy action, but of calibrated restraint.Even without rate hikes, financial conditions are already tightening at the edges:

- Rate cuts are being delayed

- Lending rates remain sticky

- Liquidity is being managed more actively

If oil prices remain elevated, these trends could deepen, gradually translating global disruptions into tighter financial conditions at home.

How Households feel the impact

For households, the effect of an oil shock is rarely immediate, but it is persistent.Fuel bills are usually the first to rise. This is followed by higher grocery costs as transportation expenses feed into food prices. Over time, borrowing costs remain elevated, delaying relief on EMIs. However, for now the government has kept the petrol and diesel prices unchanged by slashing excise duties.

Home loan EMIs stay elevatedFloating-rate borrowers see limited benefit if rate cuts are pushed back, increasing total interest outgo over the life of the loan.Costlier consumer creditCar loans, personal loans, and credit card interest rates remain high, discouraging discretionary spending.Savings see partial upsideHigher deposit rates can benefit savers, but this often coincides with slower economic momentum, which can affect income growth.

The ‘double squeeze’

The most significant pressure comes from the combination of two forces:

- Rising cost of living driven by fuel-led inflation

- Elevated borrowing costs due to delayed monetary easing

This “double squeeze” gradually compresses disposable incomes. Even without a sudden shock, the cumulative effect is visible; households spend more on essentials while financial flexibility declines.Fuel costs rise. Food becomes more expensive. EMIs remain sticky. Wage growth does not always keep pace.

From global conflict to local budgets

The current crisis is a textbook case of how tightly linked global geopolitics and domestic economics have become.A blockade in the Strait of Hormuz is not just a strategic manoeuvre, it is a disruption with global economic consequences. For India, the transmission runs through oil prices, inflation dynamics, and financial conditions before finally reaching household budgets.For now, there is no immediate shock to household finances. But if disruptions persist, the impact will not come as a sudden jolt, it will build gradually, tightening budgets over time.What begins in a narrow shipping lane thousands of kilometres away can, and often does, end up reshaping financial decisions at home.